The Coronavirus Pandemic has dramatically changed the business environment around the world.

Banks, finance companies, car manufacturers and fleet management organisations with significant exposure to auto loans and leases are readjusting their forecasts for used car prices.

In aid of this, the following report highlights our observed history of used car prices and how COVID-19 is affecting prices in the near term.

Latest Articles

- Will There Be More Car Sales in 2021?As 2020 comes to a close, we review the effects of the Coronavirus pandemic on car sales, prices and supply… Read more: Will There Be More Car Sales in 2021?

- Global Slowdown in Car Trade Fuels Stock ShortagesInternational trade in cars has reduced dramatically due to the Coronavirus Pandemic. Car Imports into Australia are down $3 billion… Read more: Global Slowdown in Car Trade Fuels Stock Shortages

- Australian Used Car Prices Bounce Back Despite COVID-19: New Datium Insights-Moody’s Analytics IndexA new index launched by Moody’s Analytics in collaboration with Datium Insights reveals that Australian wholesale used-vehicle prices increased by 10.6% from April to May of… Read more: Australian Used Car Prices Bounce Back Despite COVID-19: New Datium Insights-Moody’s Analytics Index

Effect of COVID-19 on Prices

The Great Lockdown, as it’s being called, has had a tremendous impact on business activity. This has not spared the used car market.

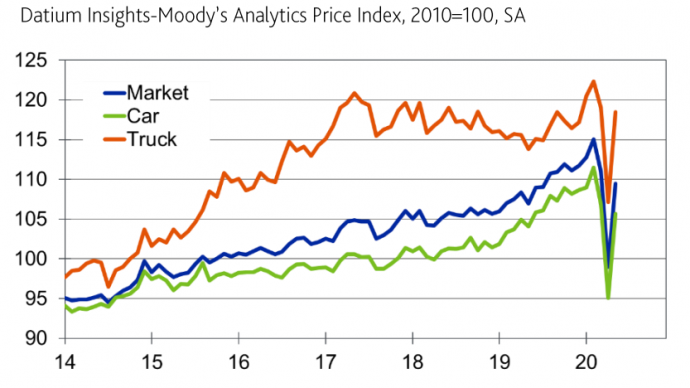

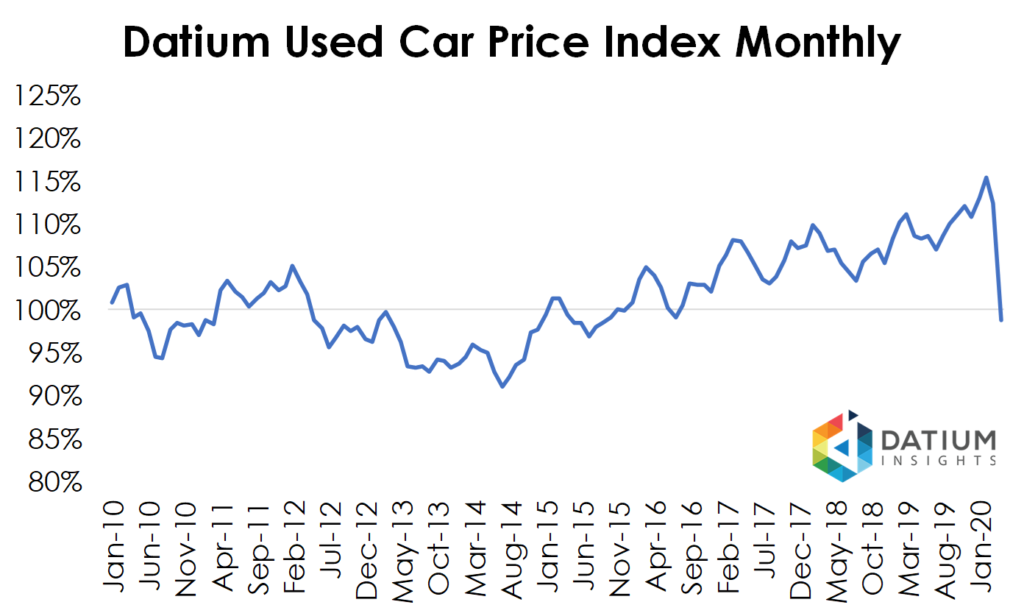

Datium Insights Used Car Market Price Indices track average used car prices for 3-year old cars through auction markets. Our data captures over 65% of activity in the auction space, providing real-time tracking of price movements.

We adjust for age, mileage and various vehicle attributes to provide a clean representation of price changes over time.

The Price Index for the total market showed a reduction of 3% in March 2020.

Australian quarantine measures largely took force halfway through March, meaning it’s effect was somewhat tempered.

A full month of social distancing in April led to a stronger fall in prices, resulting in a further 14% decline.

In total, prices fell 17% from February on wards.

Throughout the pandemic we’ve tracked the composition of cars being transacted, as well as the buyers that remained active.

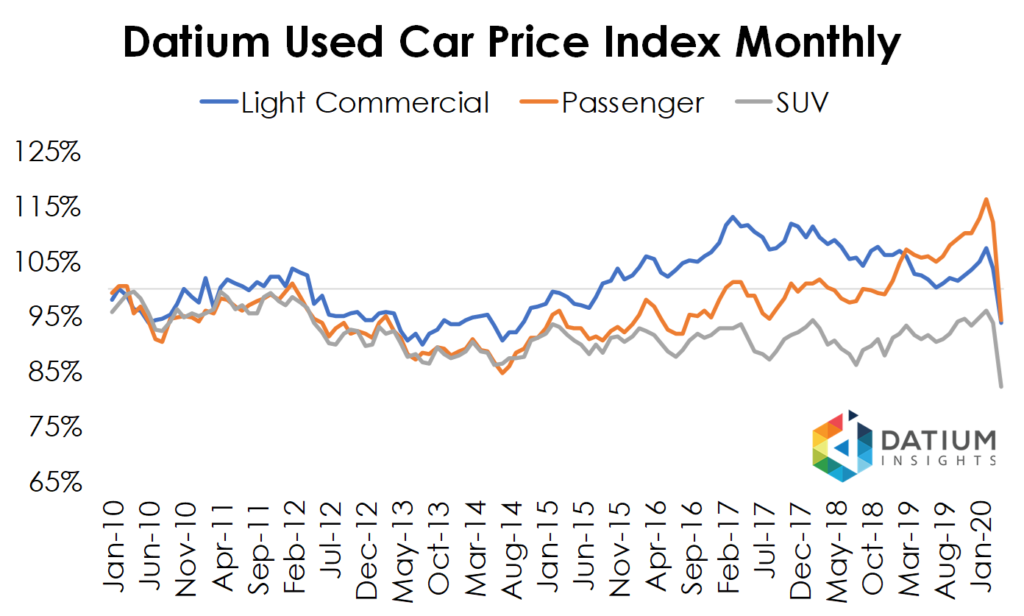

We saw light commercial vehicles and SUV’s retain their value better compared to passenger cars. Both saw price falls of 13% over March to April.

Passenger cars observed a stronger hit on prices. Demand in this space quickly shifted away from younger 3-year old cars towards older, cheaper 5-6-year-old cars.

Prices fell roughly 22% for passenger cars.

Buyer activity also shifted during this period with dealer participation falling significantly by 24%.

With foot traffic becoming non-existent, dealerships pulled back on purchasing used car stock.

COVID-19 cases began falling into single digits across the country towards the end of April. As a result, federal and state governments began slowly relaxing restrictions in each jurisdiction.

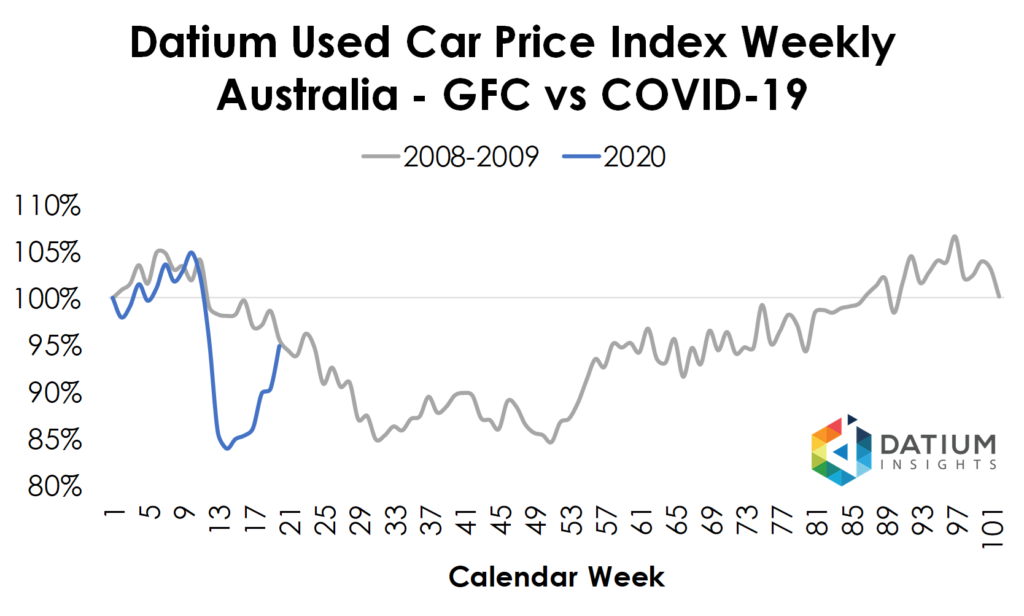

While it may seem the market is continuing to deteriorate, our weekly indices have uncovered a softening in prices. This coincides with heightened participation by dealers and an increase in overall buying activity in the latter half of April.

Prices have still remained suppressed however, with sellers being cautious about the stock they release to market.

What History Has Taught Us

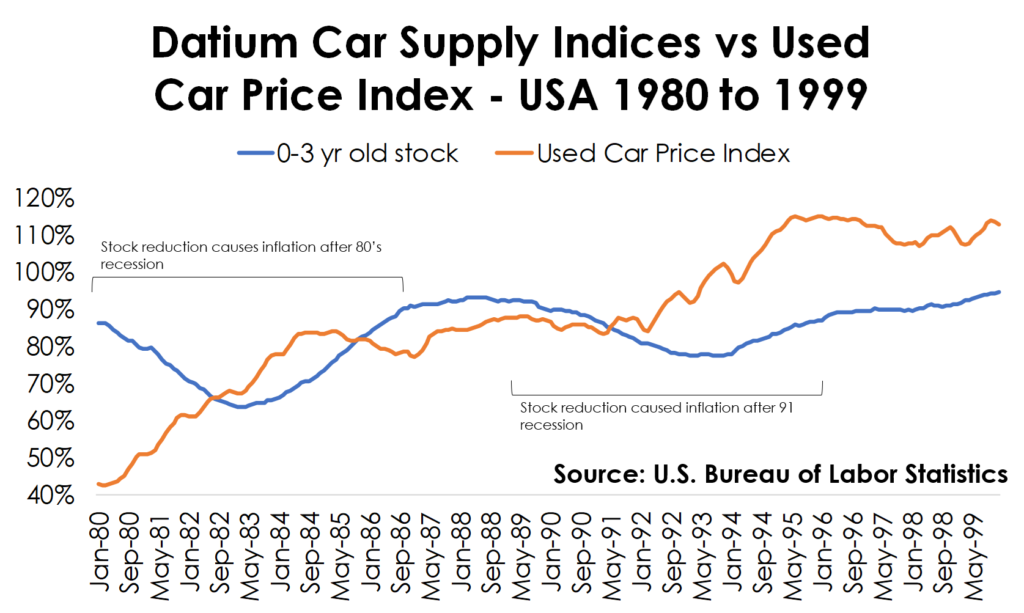

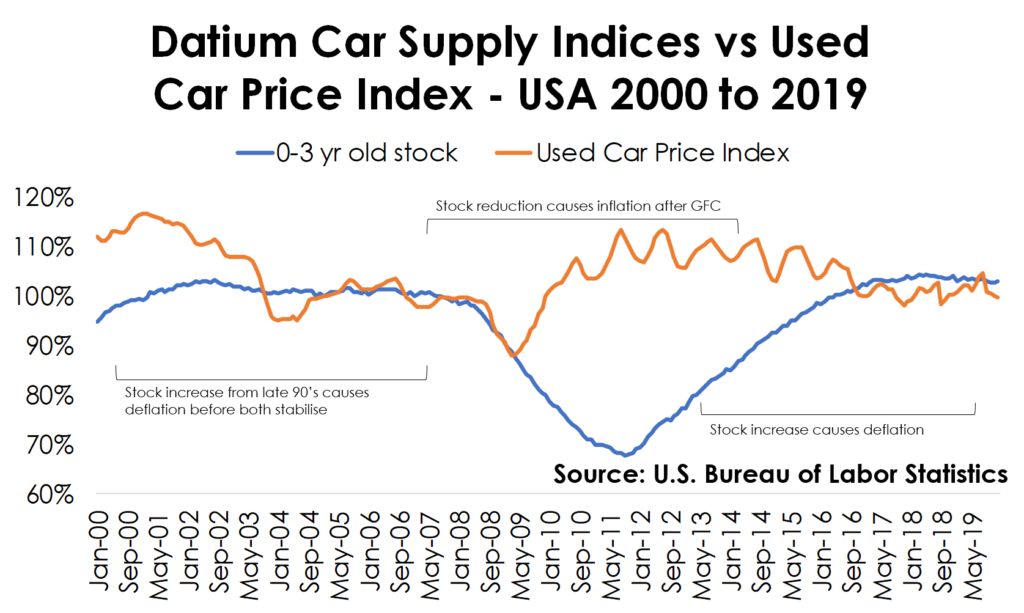

As Australia hasn’t faced a recession in over 30 years, we look to data from the US.

The Global Financial Crisis and prior recessions allow us to draw important implications for what to expect in Australia.

In the US, used car stock saw rapid decline during and after the immediate aftermath of the GFC.

Our Car Supply Indices show stock of cars under 3 years old reduced by 30% from July 2008 to July 2011.

This followed near-identical behaviour after the early 80’s and 90’s recessions.

This is due to sharp reductions in new car purchases, resulting in less stock entering the used market.

While the US saw prices fall in the immediate aftermath of the GFC, they gradually recovered to a norm as supply and demand returned to a balance.

This downturn and subsequent recovery took roughly 2 years to occur.

Australian Used Car Supply

In Australia, we’ve actually seen used car stock decline prior to the current economic crisis. This is due to an ongoing slump in new car sales.

After decades of consistent year on year growth, the market has seen two subsequent years of decline.

With a full month of social distancing restrictions, April saw the largest decline in new car sales (48.5%) since records started being kept in 1991.

Our Car Supply Indices show stock of cars under 3 years old had already declined by 10% from June 2018 to April 2020.

Our modelling predicts this figure to decline a further 18% over the next 12 months. After 12 months we expect to see a recovery ensue.

Because Australia has already seen used car stock supply shrink, this will provide a buffer to prices falling further.

Price Rebound

Given Australia’s comparably positive response to the COVID-19 pandemic, business operating environments are expected to return to norms ahead of most other nations across the world.

As people gradually gain confidence back in travel and movement, we expect buyer activity to return to normal levels. This is something we’ve already observed in late April.

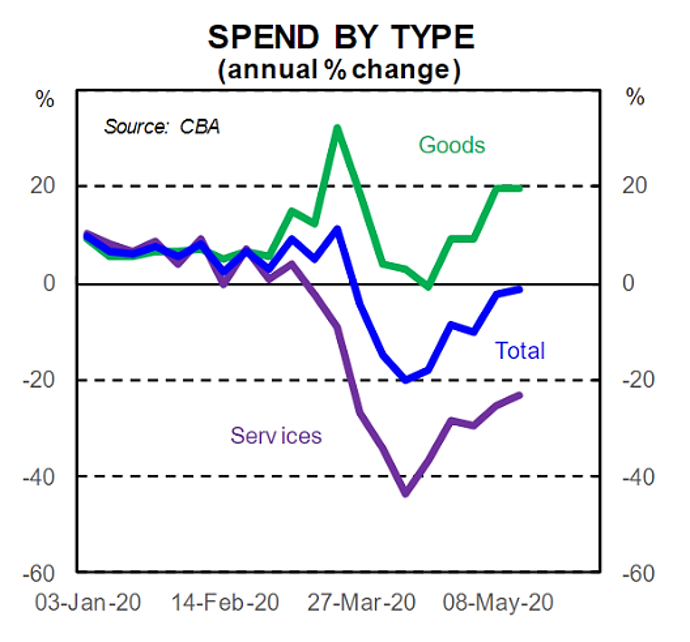

With social distancing easing in May, prices have seen a strong rebound effect. Nearly half of what was lost since February has recovered.

This follows similar recoveries in consumer spending reported by the Commonwealth Bank. CBA data found spending till May 15 to be only 2% below levels for the same time last year.

Economic Deterioration

In our view however these positive signs are a rebound from the effects of social distancing restrictions in place the past few months.

With restrictions gradually easing and fears of Coronavirus infections waning, people have naturally increased spending after foregoing purchases in late March and early April.

The deterioration of the global economy and its effects on business and consumer activity are only beginning to take effect.

Over 36 million new unemployment claims have been filed in the US, a level that is unprecedented in recorded history. This follows statements by the US Federal Reserve that US unemployment could reach 25%, on par with the Great Depression.

Jobless claims in the U.K. increased to over 2 million according to the U.K. Office for National Statistics, while Japan has already fallen into recession.

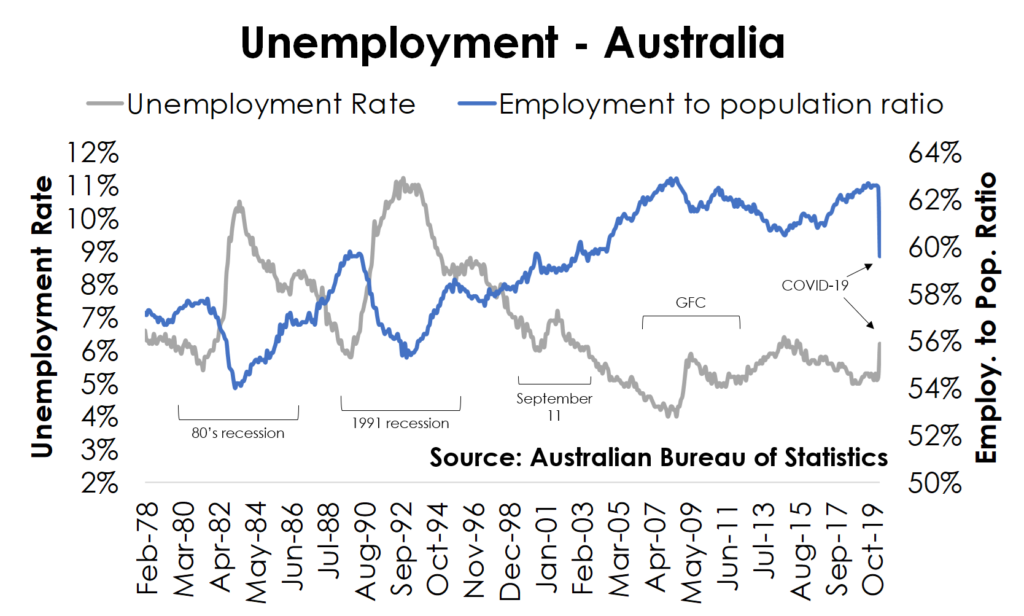

In Australia, our unemployment rate is predicted to increase to a peak of 10%. Considering past recessionary experiences and the magnitude of the Coronavirus pandemic, this prediction is likely optimistic.

The unemployment rate in Australia increased to 6.3% in April – an unassuming small increase given the historic events that have taken place.

However, this actually is not an accurate picture due to quirks in the way our unemployment rate is calculated.

When combining the millions of people who have either left the labour force entirely, are receiving JobKeeper payments despite not actually working, or are currently underemployed , a truer picture puts our actual unemployment rate closer to 20%.

Timeline to a Recovery

The downstream effects of this spike in unemployment will undoubtedly result in Australians increasing their savings and reducing their spending.

The full effect on business activity is likely to be felt over the coming months as people movement resumes to normal levels.

The GFC caused prices to fall 15% over the course of 12 months. This is despite Australia not actually entering a recession during that time.

While prices have seen a strong recovery so far in May, there is a strong possibility that the impending recession will reverse this recovery, leading to volatility in prices over the next 6 months.

Despite tightening of used car stock, a number of factors could potentially cause prices to deteriorate over the coming months:

- threat of a rebound in virus transmission and resumption of social distancing restrictions

- used car prices generally see a dip in winter, in line with behaviour in other assets classes

- changes in unemployment and spending will reduce demand for motor vehicles overall across the next 12 months

- repossession activity is likely to pick up later in the year, after relief and hardship packages have been exhausted

As a result, we predict an elongated ‘U’ shaped recovery for used car prices, seeing 12 months of volatility before an eventual recovery ensues.

Barring any large-scale recurrence of virus transmission, our modelling predicts prices to recover by the end of 2021 before eventually returning to pre-COVID norms in mid-2022.

By Tanim Ahmed, Head of Product at Datium Insights

Tanim is a Macquarie University alumni with degrees in Finance and Economics. He has spent a decade in the Leasing and Finance industry, specializing in Residual Value risk.

Please contact Datium Insights for further analytical support and advisory services.

Sources: https://fred.stlouisfed.org, https://www.ons.gov.uk, https://www.abs.gov.au, https://www.commbank.com.au

Disclaimer: This is a general information service only and we do not provide advice or take into account your personal circumstances, financial situation or needs. Please seek professional advice with regards to how any of the material on this website can impact your own financial situation. Datium Insights is not liable for any loss caused, whether due to negligence or otherwise arising from the use of, or reliance on, the information provided directly or indirectly, by use of this website.

Australian Used Car Prices Bounce Back Despite COVID-19: New Datium Insights-Moody’s Analytics Index

Australian Used Car Prices Bounce Back Despite COVID-19: New Datium Insights-Moody’s Analytics Index